The Great Wealth Transfer is often reduced to a simple idea: older generations will pass down trillions, younger generations are more digitally native, and digital assets should benefit. That framing is neat, but it misses the bigger story.

What matters is not just that wealth is changing hands, but that it is happening at the same time finance itself is becoming more digital, more tokenised, and more connected to 24/7 markets.

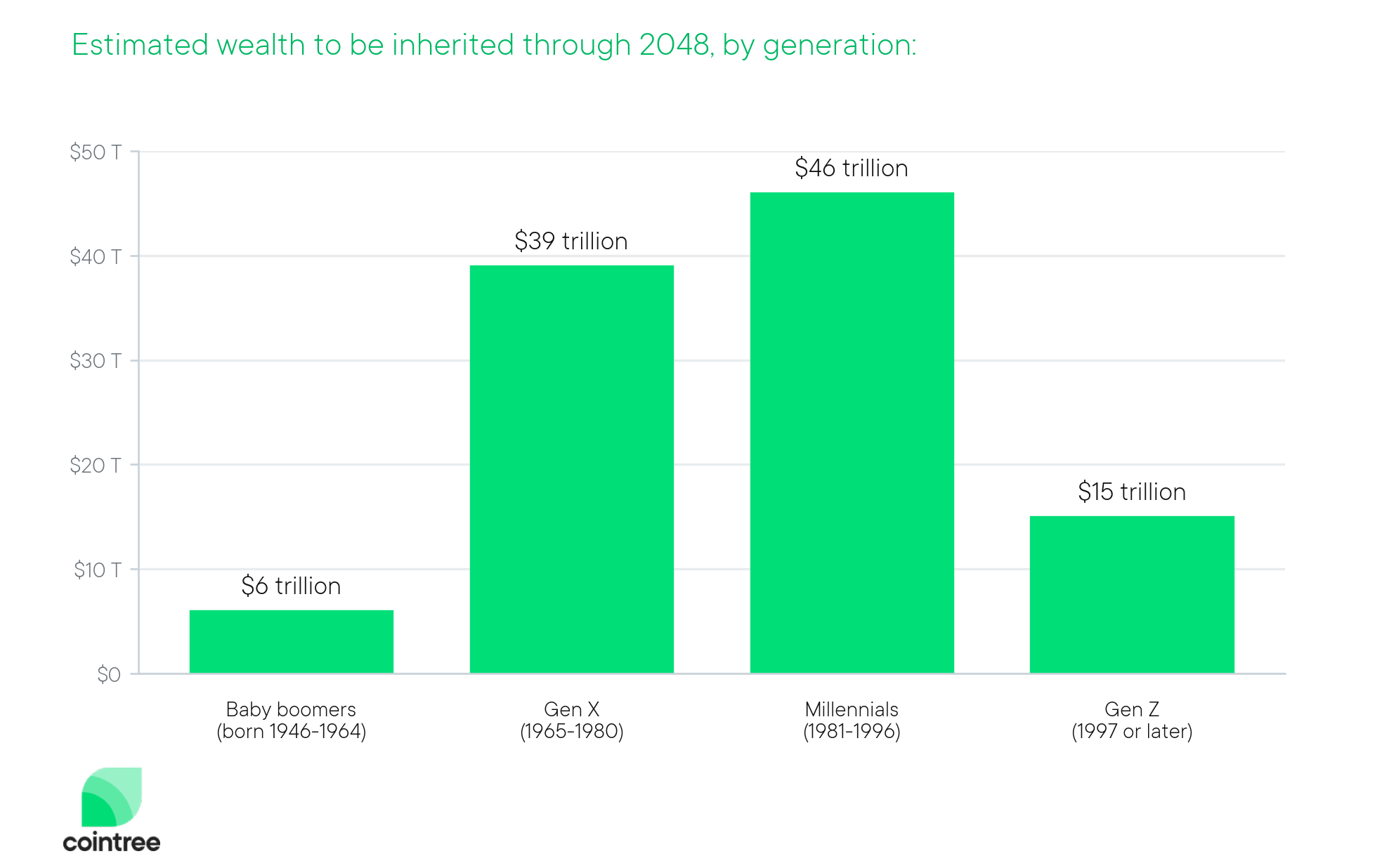

First up, the numbers are huge

In the U.S., Cerulli projects US$124 trillion will transfer through 2048, including US$105 trillion to heirs and US$18 trillion to charity. It also says US$54 trillion is expected to transfer first to spouses, with nearly US$40 trillion of those spousal transfers going to widowed women. This is not a niche wealth-planning trend. It is one of the largest capital handoffs in history.

Source: Data: Cerulli Associates 2024 report

Australia has its own version of the same story. JBWere says total inheritances were about A$150 billion in 2024 and estimates roughly A$5.4 trillion will be passed on over the next 20 years. The older benchmark commonly referenced in Australia was around A$3.5 trillion over 20 years, based on earlier Productivity Commission-era work.

Translation: a lot of money is moving.

It probably does not go straight into Bitcoin

This is where the simple take falls apart.

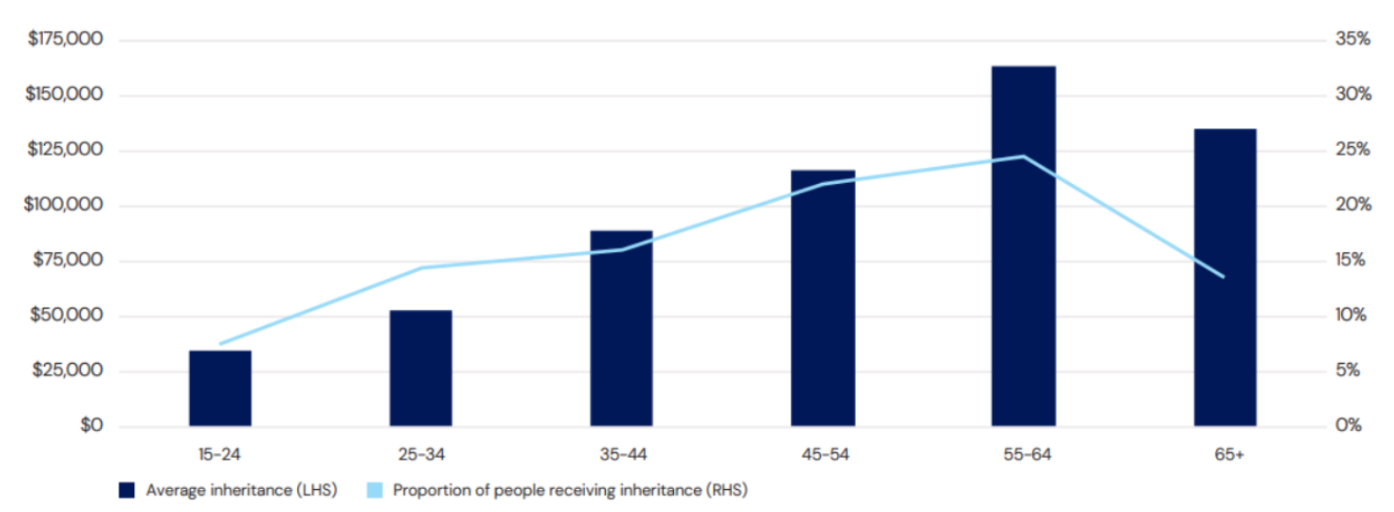

Most inheritances do not land in the hands of 24-year-olds looking for the next meme coin. In Australia, the Productivity Commission says inheritance recipients are around 50 on average, and JBWere points to inheritances peaking around age 60. That usually means people are thinking about debt, retirement, income, family, and capital preservation, not just risk-on punts.

Source: JBWere-Bequest-Report

That is why the better thesis is not “inheritance money pumps crypto”. The better thesis is this:

A growing share of wealth is moving into the hands of people who are more comfortable with digital finance, app-based investing, online money movement, and markets that do not shut for the weekend. That is not automatically bullish for every token. But it is a meaningful long-term tailwind for digital assets, tokenised products, and onchain rails.

Australia is a sneaky-good case study for this

Why? Because a huge amount of wealth here already sits inside long-duration financial structures.

APRA says Australian superannuation assets reached A$4.4855 trillion at 31 December 2025, with A$3.1814 trillion in APRA-regulated funds and A$1.0614 trillion in SMSFs. Contributions over the year hit A$220.8 billion. On top of that, ABS data shows household net worth rises across the life cycle and peaks at about A$1.835 million for households aged 65 to 69.

That matters because it means the wealth transfer story is not just about cash. It is about property, super, investment portfolios, private wealth, and how all of that may eventually interact with more digital market infrastructure.

The rails are already being built

This is the part that makes the whole thing pop.

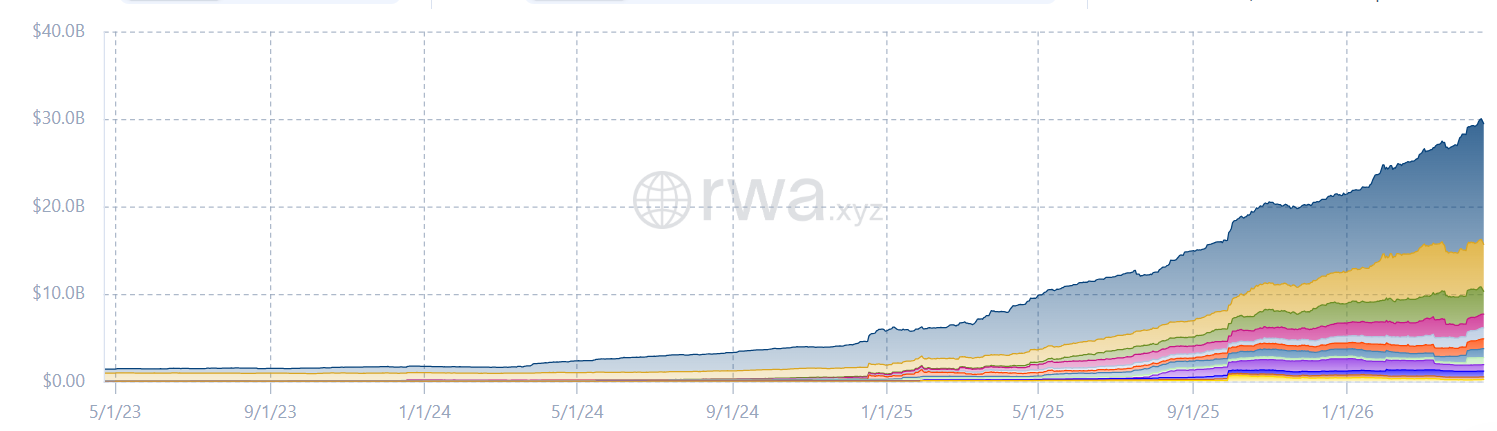

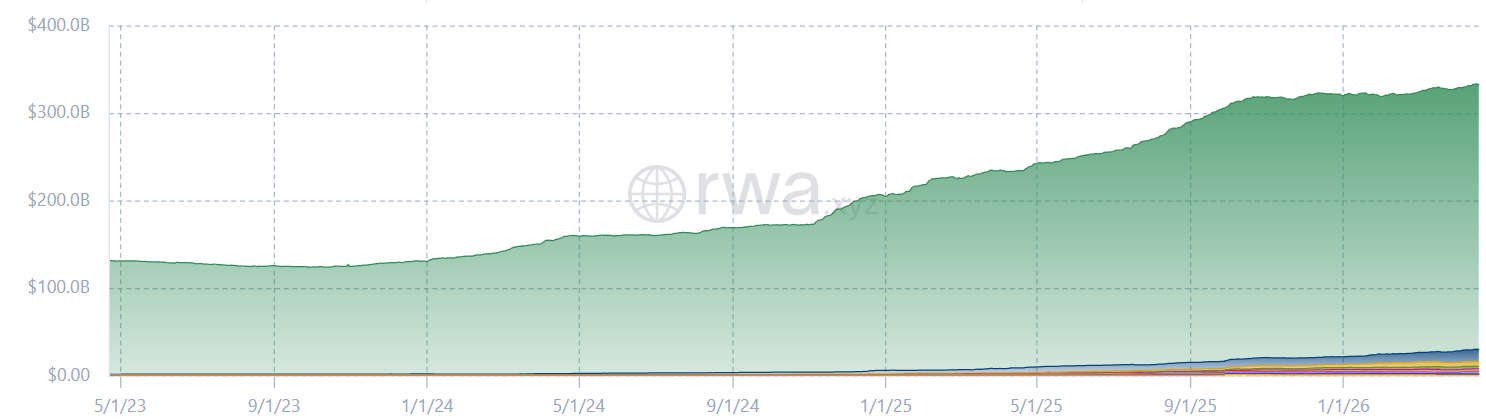

RWA.xyz shows US$8.75 trillion in monthly stablecoin transfer volume, US$300+ billion in stablecoin market cap on its stablecoin page, and 239.08 million holders as of 12 March 2026. On its treasuries page, tokenised U.S. Treasuries sit at US$12.06 billion with 55,144 holders.

Total RWA Value- $26 Billion:

Add in stablecoins and that number jumps to $340 Billion:

Circle reported US$75.3 billion of USDC in circulation at the end of 2025, plus US$11.9 trillion in USDC on-chain transaction volume in Q4 2025 alone. That is not an experiment anymore. That is scale.

The idea that TradFi is ignoring crypto looks more tired by the month. Mastercard said in April 2025 that it was rolling out end-to-end stablecoin payment capabilities, including wallet enablement, merchant settlement, and on-chain remittances. Then in March 2026, Reuters reported Mastercard agreed to buy stablecoin infrastructure firm BVNK for up to US$1.8 billion to deepen its push into blockchain-based money movement.

Now add the Generational Angle

Gallup says 14% of U.S. adults own crypto, with ownership significantly higher among men aged 18 to 49 at 25%. Reuters also reported that Gen Z workers begin contributing to workplace retirement plans at an average age of 23, versus 28 for millennials. So younger cohorts are not just more online. They are also engaging with investing earlier.

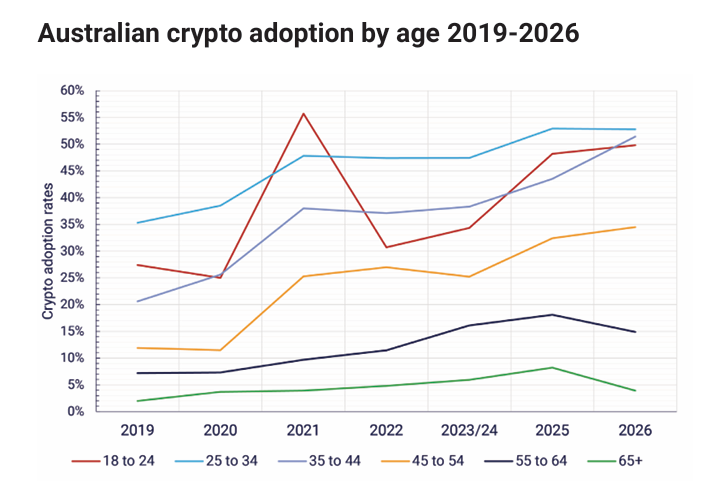

In Australia, ASIC says 23% of Gen Z now have crypto assets, up from 9% in 2023. Independent Reserve’s 2025 Cryptocurrency Index found 31% of Australians have invested in or held crypto, with 95% awareness while the same release also said 32.5% of Australians currently own, or have previously owned, crypto.

Source: Independent reserve IRCI 2026

That is the real unlock.

Not everyone needs to become a full-time crypto person. They just need to get comfortable with digital assets as a category. Once that happens, the jump to stablecoins, tokenised funds, tokenised bonds, onchain settlement, and 24/7 financial products gets much smaller.

So what is actually bullish here?

Not a single “boomers die, crypto flies” moment. It is something slower, and probably more durable.

Over time, a larger share of global wealth will be controlled by people who are more comfortable living in a digital financial world. At the same time, the assets themselves are becoming more digital, more programmable, and more portable across always-on rails. Stablecoins are scaling. Tokenised treasuries are scaling. Payments giants are plugging in. Super pools are enormous. And younger cohorts are already more open to digital assets than the generations before them.

That does not guarantee that inherited wealth flows directly into crypto. But it does make one thing pretty clear:

The Great Wealth Transfer is happening at the same time finance is going digital and that is a very interesting setup for crypto rails.

This article is for general information only and does not constitute financial advice. It does not take into account your personal objectives, financial situation, or needs. Digital assets can be volatile and involve risk.