Australia’s New Budget Could Change How Crypto Investors Build Wealth

Australia’s latest Federal Budget included a major change that could reshape how investors think about crypto, shares, ETFs and property.

From 1 July 2027, the Government plans to replace the current 50% capital gains tax discount with a new system based on inflation indexation. It will also introduce a minimum 30% tax on capital gains.

According to the Budget, these CGT reforms will only apply to gains arising after 1 July 2027. Investors in new builds will also be able to choose between the current 50% CGT discount or the new arrangements.

It sounds technical, but the simple takeaway is this:

If you invest in assets that rise faster than inflation, you may pay more tax when you sell.

And yes, that includes crypto.

How does CGT work right now?

Under the current system, Australian investors who hold an asset for more than 12 months may be eligible for a 50% CGT discount.

For example, if someone buys Bitcoin for $50,000 and later sells it for $110,000, they have made a $60,000 capital gain.

Under the current system, only half of that gain, or $30,000, is generally added to their taxable income.

This system has been important for long-term investors because it rewards patience. It applies across many assets, including crypto, shares, ETFs and investment property.

What changes under the new system?

The new model works differently. Instead of cutting the taxable gain in half, the Government plans to let investors increase their cost base by inflation. In theory, this means investors are only taxed on their “real” gain after inflation.

For slower-growing assets, that may not sound too bad. For higher-growth assets, the difference can be much bigger.

If an asset rises 30%, 40% or 50% per year, a small CPI adjustment may not make much difference. The taxable gain can still be large, and without the 50% discount, the final tax bill may be higher.

That is why this change matters for crypto investors. Bitcoin and other digital assets can be far more volatile than traditional assets, but they have also historically gone through periods of very strong growth. Under an inflation-indexed system, more of those gains may be taxable compared with today’s rules.

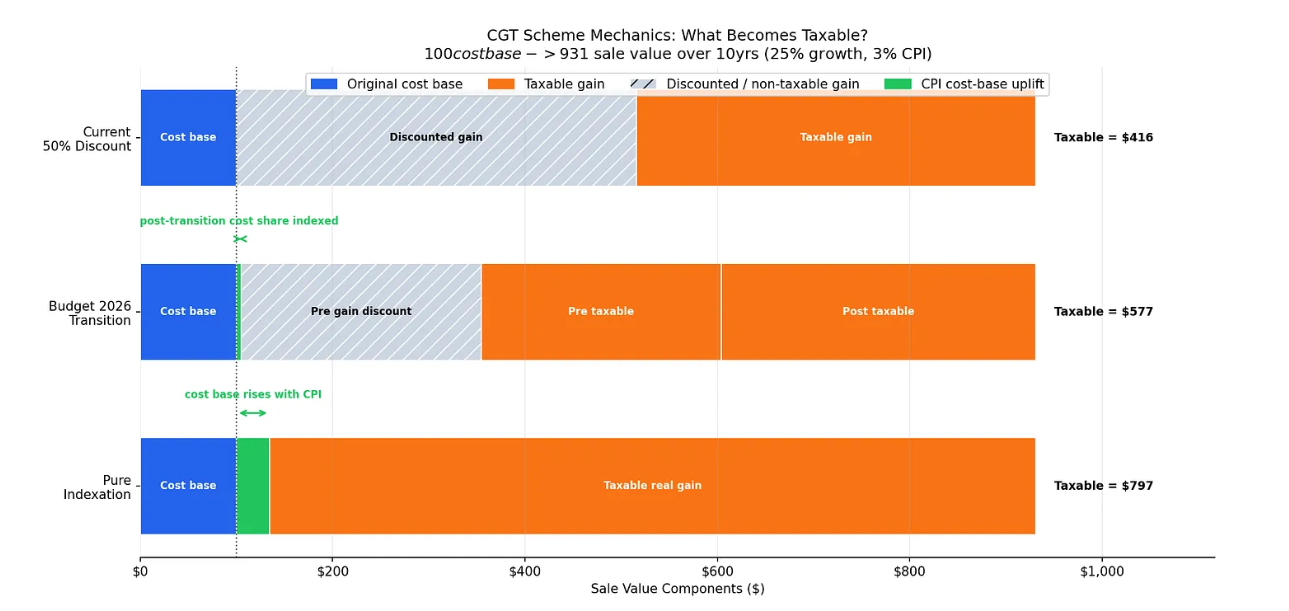

Checkonchain’s analysis makes a similar point, arguing that replacing the 50% CGT discount with CPI indexation could increase the effective CGT burden for higher-growth assets.

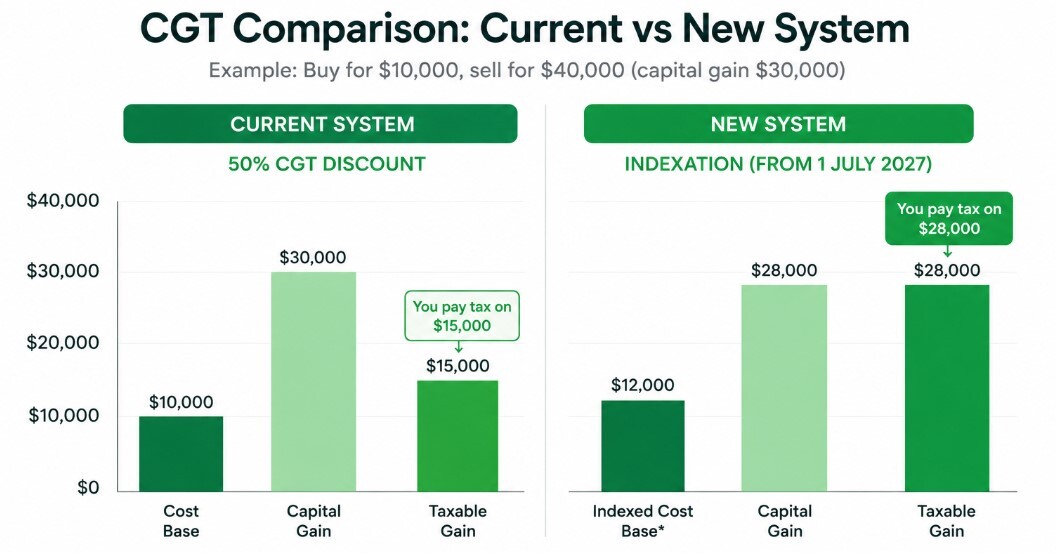

A simple crypto example

Let’s say an Australian buys $10,000 of Bitcoin and holds it for several years.

If that Bitcoin later becomes worth $40,000, the gain is $30,000.

Under today’s rules, if they held the Bitcoin for more than 12 months, they may be eligible for the 50% CGT discount.

That means only $15,000 of the gain would generally be taxable.

Under the proposed new system from 1 July 2027, the 50% discount would be replaced with cost base indexation. Instead of halving the taxable gain, the original purchase price would be adjusted upward by inflation.

For example, if inflation lifted the original $10,000 cost base to $12,000, the taxable gain would be calculated like this:

Sale price: $40,000

Indexed cost base: $12,000

Taxable gain: $28,000

So in this simple example:

Current system: $15,000 taxable gain

New system: $28,000 taxable gain

That does not automatically mean someone pays tax on the full $28,000 at the same rate. Their final tax bill would still depend on their income, marginal tax rate, dates, cost base and personal circumstances, but it shows the main difference.

The current system gives investors a large discount after 12 months, the new system adjusts the cost base for inflation.

For assets that only rise slightly above inflation, indexation may help. But for high-growth assets like Bitcoin, the current 50% CGT discount may have been much more valuable.

Source: checkonchain

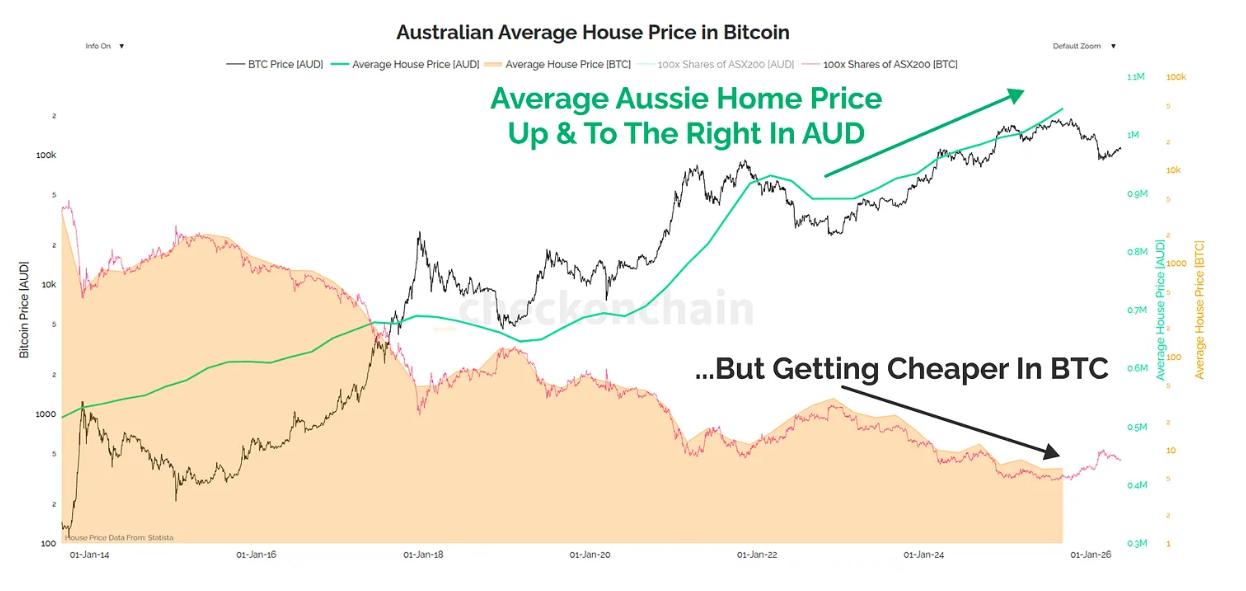

Why this matters for younger Australians

This change is being framed largely around housing affordability, but the CGT changes are not only about property. The Budget says the Government will replace the 50% CGT discount with an inflation-based discount, and that investors with gains well above inflation will pay more.

That means shares, ETFs and crypto are also part of the conversation. For many younger Australians, buying a home is already difficult. Saving a deposit in cash alone can be slow, especially when house prices, rent and living costs keep rising.

That is why some younger investors use assets like ETFs, shares or crypto to try and grow their savings over time.

Those assets are not risk-free, crypto in particular can be highly volatile, but changes to CGT can still affect the path people use to build wealth before they even get to the property market.

If the tax system takes a bigger bite out of high-growth investments, it may become harder for some Australians to turn investment gains into a home deposit.

Source: checkonchain

What about property?

The Budget also includes changes designed to push more investment toward new housing supply.

The Government says the reforms are intended to help more Australians own their own home, with changes to negative gearing and capital gains tax concessions estimated to support around 75,000 additional homeowners over the decade.

It is also establishing a $2 billion Local Infrastructure Fund to support infrastructure for up to 65,000 homes over the decade.

The policy goal is clear: make new housing more attractive and reduce some of the tax advantages attached to existing property investment.

If people use shares, ETFs or crypto to save for a deposit, the CGT changes could reduce their after-tax returns when they eventually sell. So, while the policy may help on one side of the housing equation, it could make the saving journey harder on the other.

Why crypto investors should pay attention

Crypto investors are used to volatility, tax changes are different. They can change the final outcome even if the investment thesis stays the same.

A Bitcoin investor may still be right about long-term adoption, scarcity or digital asset growth. But if the tax treatment changes, the amount they actually keep after selling may change too.

That matters for anyone using crypto to save for a major goal, such as buying a home, funding education, building long-term wealth, diversifying outside cash and property, or growing an SMSF portfolio.

Record keeping will also become more important. Investors may need to pay closer attention to when they bought an asset, what their cost base was, what the asset was worth around the transition date, and how much of the gain happened before and after 1 July 2027.

Crypto tax reporting is already detailed. These changes could make it even more important to stay organised.

When do the changes start?

The key date is 1 July 2027.

The Budget says the CGT reforms will only apply to gains arising after this date.

That means gains before then are expected to be treated under the current rules, while gains after then would fall under the new approach.

For investors who already hold crypto, shares or property, the timing of future gains could become more important. For investors buying after the changes take effect, the new system may become the default way future capital gains are calculated.

The bigger picture

This Budget is not just about crypto, it is about how Australia taxes investing.

For property investors, it changes the way future gains may be treated.

For share and ETF investors, it changes the long-term wealth-building equation.

For crypto investors, it matters because digital assets often sit at the high-growth, high-volatility end of the investment spectrum.

And for young Australians, it raises a bigger question:

If housing is already hard to reach, what happens when the assets people use to save for a deposit are taxed differently too?

The final impact will depend on each person’s income, assets, holding period, inflation and future returns, but the direction is clear: Australia’s investment rules are changing, and crypto investors should be paying attention.

This article is general information only and does not consider your personal circumstances. Speak with a registered tax professional for advice specific to your situation.